As the year-end approaches, LGBT people, whether single, in domestic partnerships, or married, will want to focus on their investment planning and on the implications for their tax filings next April. Important issues merit your attention before 2013 draws to a close. Relationship status matters, and the follow checklists for November and December cover important considerations — though, of course, they are not the be all and end all:

Checklists for LGBT people who are single, in domestic partnerships, or married

SINGLE LGBT PEOPLE

November

Develop a plan to complete charitable and family member gifts by year-end. Also consider opening, funding, or adding to 401K accounts, IRA accounts, and 529 accounts. Remember to look at all of your retirement accounts, including accounts from previous jobs.

Look at your accounts and discuss your beneficiary designations with your financial advisor and attorney; make any necessary adjustments due to life changes (marriage, divorce, birth of child, death, disability, etc.) or changes in your goals.

Medical: Make sure to enroll in your health plan. Also nominate someone to make medical decisions for you if you are incapacitated.

December Financial: Fully fund your IRA and/ or your employer retirement accounts. Check with your accountant to confirm that you have dealt with ALL your retirement accounts.

Review the beneficiary you have selected for EACH retirement account to make sure you have the correct beneficiary on each account.

When selling securities you own, remember the trade date, not the settlement date, determines the year of the sale and recognition of any gain or loss in most situations.

Make sure any 529 distribution or an Education Savings Account (ESA) distribution and actual payment of qualified education expenses occur in the same tax year.

Take required minimum distributions (RMDs) before December 31. An RMD for your IRA cannot be combined with an RMD for your employer plan. Each must be calculated and distributed separately.

If you’ll reach age 65 or plan to retire in 2014, make an appointment to talk with your local Social Security Administration office early in January to discuss Medicare and Social Security claiming options.

Personal: Review leases and checking accounts to see that you are set up correctly.

UNMARRIED LGBT PEOPLE IN RELATIONSHIPS

November

Develop a plan to complete charitable and family member gifts by year-end. Also consider opening, funding, or adding to 401K accounts, IRA accounts, and 529 accounts. Remember to look at all of your retirement accounts including accounts from previous jobs.

Look at your accounts and discuss your beneficiary designations with your financial advisor and attorney; make any necessary adjustments due to life changes (marriage, divorce, birth of child, death, disability, etc.) or changes in your goals.

Medical: Make sure to enroll in your health plan. Also nominate someone to make medical decisions for you if you are incapacitated.

Check with your or your partner’s health plan to see if you qualify for Domestic Partnership Medical benefits.

December Financial: Fully fund your IRA and/ or your employer retirement accounts.

Review the beneficiary you have selected for EACH retirement account to make sure you have the correct beneficiary on each account.

When selling securities you own, remember the trade date, not the settlement date, determines the year of the sale and recognition of any gain or loss in most situations.

Make sure any 529 distribution or an Education Savings Account (ESA) distribution and actual payment of qualified education expenses occur in the same tax year.

Take required minimum distributions (RMDs) before December 31. An RMD for your IRA cannot be combined with an RMD for your employer plan. Each must be calculated and distributed separately.

If you’ll reach age 65 or plan to retire in 2014, make an appointment to talk with your local Social Security Administration office early in January to discuss Medicare and Social Security claiming options.

Personal: Review leases and checking accounts to see that you are set up correctly.

MARRIED LGBT COUPLES:

November Personal: Go over your respective accountants, lawyers, and other financial professionals including financial advisors and agree if you are going to proceed as “ours” or as “yours, mine , ours.”

Financial: Have a written agreement as to how bank and brokerage accounts are to be registered.

Notify banks and brokerage firms IN WRITING of any registration changes in your accounts.

Check with your accountant NOW to see if you should be filing jointly or separately.

Look at your portfolios and see if you should sell securities to establish losses. Remember, the last day to double up your position to avoid a wash sale is Friday, November 29, 2013.

Develop a plan to complete charitable and family member gifts by year-end. Also consider opening, funding, or adding to 401K accounts, IRA accounts, and 529 accounts. Remember to look at all of your retirement accounts including accounts from previous jobs.

Look at your accounts and discuss your beneficiary designations with your financial advisor and attorney; make any necessary adjustments due to life changes. After marriage you need to update your beneficiary information on your accounts—it is not automatically updated.

Review your financial goals and budgets.

Update wills.

Medical: Make sure to enroll in your health plan. Also nominate someone to make medical decisions for you if you are incapacitated.

Review both your Medical plans to see which one fits your needs best or if you want to keep your individual plans.

December Financial: Fully fund your IRA and/ or your employer retirement accounts.

Review and update the beneficiary you have selected for EACH retirement account to make sure you have the correct beneficiary on each account.

When selling securities you own, remember the trade date, not the settlement date, determines the year of the sale and recognition of any gain or loss in most situations.

Make sure any 529 distribution or an Education Savings Account (ESA) distribution and actual payment of qualified education expenses occur in the same tax year.

Take required minimum distributions (RMDs) before December 31. An RMD for your IRA cannot be combined with an RMD for your employer plan. Each must be calculated and distributed separately.

If you’ll reach age 65 or plan to retire in 2014, make an appointment to talk with your local Social Security Administration office early in January to discuss Medicare and Social Security claiming options.

Personal: Review leases and checking accounts to see that you are set up correctly.

Go over all real estate holdings.

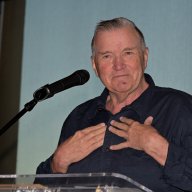

Leonard Boccia is a Chartered Retirement Planning Counselor® and Managing Director-Investments in the Boccia & Quinn Wealth Management Group of Wells Fargo Advisors. Wells Fargo Advisors is not a tax or legal advisor and Wells Fargo Advisors, LLC is a Member of the SIPC. Investment and insurance products are NOT FDIC-Insured. there is NO Bank Guarantee, and they MAY Lose Value. Boccia can be reached at Leonard.Boccia@wellsfargoadvisors.com or 212-205-2946.